Periods of heightened uncertainty often coincide with low, or even negative, stock-bond correlation, reinforcing the need for portfolio diversification.

Global equity markets regained some composure in May as the announcement of reduced tariff rates between the U.S. and China revived hopes for a de-escalation in trade tensions. The U.S. Court of International Trade’s decision to block reciprocal tariffs added further optimism, despite the appeals court ruling allowing tariffs to remain temporarily. However, global bond markets are increasingly worried about the deteriorating fiscal deficits and long-term sustainability in the U.S. and elsewhere. Consequently, while the MSCI World index and MSCI Emerging Market index posted gains of 6.0% and 3.2%, respectively, the Bloomberg Global Aggregate index ended the month down -0.4%, all in local currency total return terms.

In Australia, the 30-year government bond yields rose 14 basis points (bps) over the month to 4.95%, as the dominant outcome from the Federal Election pointed towards a looser fiscal stance from the re-elected Australian Labour Party. That said, these policies were previously outlined in the Budget and the Reserve Bank of Australia (RBA) also delivered a dovish rate cut at the May meeting, which eased some pressure on bond yields. The back-up in long-end yields was more pronounced in other developed markets.

In the U.S., 30-year treasury yields surged 22 bps to 4.9% by the end of the month, after briefly testing the 5%-mark intra-month. The weak 20-year auction and Moody’s downgrade of U.S. government debt were challenges, though market concerns were primarily centered on the House’s narrow passage of the Budget reconciliation bill. Details were largely as expected, but the sheer size of additional estimated increase in the deficit (USD 2.8-3.8 trillion over a decade) if the Senate passes the bill, raises significant concerns over the U.S.’s fiscal sustainability, prompting bond investors to demand greater compensation and steepening the yield curve through a higher term premium.

Japan also witnessed a sharp pick-up in its 30-year government bond yields, which climbed 24 bps to a record-high at 2.9%. Fiscal health remains a concern amid government tensions over reducing consumption tax, although Japan Prime Minister Ishiba's emphasis on fiscal discipline may alleviate some pressure on yields amidst the Bank of Japan’s (BoJ’s) tapering plans. The upcoming monetary policy meeting in June will be crucial for monitoring the central bank’s potential changes to its purchasing pace. On the other hand, China's monetary policies were notably loosened, with the central bank lowering policy rates, reducing reserve requirement ratios to inject liquidity, and expanding relending programs to targeted sectors, all aimed at bolstering domestic growth.

With uncertainties surrounding trade policies persisting and remaining volatile, much like U.S. President Trump’s 50% tariff announcement on the European Union, which was postponed just two days later, fiscal policy uncertainties are further obscuring visibility for the year ahead. Nonetheless, a silver lining emerges, as periods of heightened uncertainty often coincide with low, or even negative, stock-bond correlation, reinforcing the need for portfolio diversification.

Australian economy

- The Australian Labour Party (ALP) has been re-elected in the federal election, with Anthony Albanese becoming the first prime minister to win a second term since 2004. The ALP has gained additional seats in both the lower house, with an outright majority, and the Senate, which will require the Green party or independents to pass legislations. Fiscal policies are expected to support growth with a rising deficit, as outlined in March’s Budget, with most measures already legislated.

- The RBA lowered the cash rate by 25 bps to 3.85% at the May meeting. The policy statement and press conference were noticeably more dovish than before. Upside risks to inflation are now considered to have “diminished”, with growth and inflation forecasts both revised lower. With the 25bps cut being a consensus decision and fully priced in, Governor Bullock noted that a 50bps cut was discussed by the Board, affirming a dovish pivot at this meeting.

- The monthly consumer price index (CPI) stood at 2.4% year-over-year (y/y) in April, a touch above consensus estimates. Strength was driven by seasonal holiday prices and annual increases in health insurance premiums. Trimmed mean inflation rate edged up to 2.8% y/y but remains within the RBA’s 2%-3% target band.

(GTM AUS page 6) - Wage growth also rose to 3.4% y/y in 1Q, reflecting higher pay for private aged care and childcare workers as mandated by the government, though wage growth in other sectors slowed. Total employment increased 89k in April, above consensus estimates, while unemployment rate remained at 4.1% and the participation rate rose to 67.1%.

(GTM AUS page 9) - Retail sales expanded 0.3% month-over-month (m/m) in March, though likely boosted by household stockpiling ahead of adverse weather in Queensland.

- Consumer sentiment improved slightly in May, with the index up 2.2% to 92.1, as driven by a rebound in financial markets and a clear-cut Federal election result.

(GTM AUS page 6) - Business conditions declined further in April to the lowest level since 2020, although confidence edged up.

(GTM AUS page 8)

Equities

- The ASX 200 rose 4.2% in May, as markets cheered on the RBA’s dovish rate cut, easing trade tensions between the U.S. and China, and a renewed hope for a soft-landing outlook. All sectors delivered positive returns over the month, led by Technology (+19.2%) and Energy (+8.6%), while Utilities (0.3%) was the laggard.

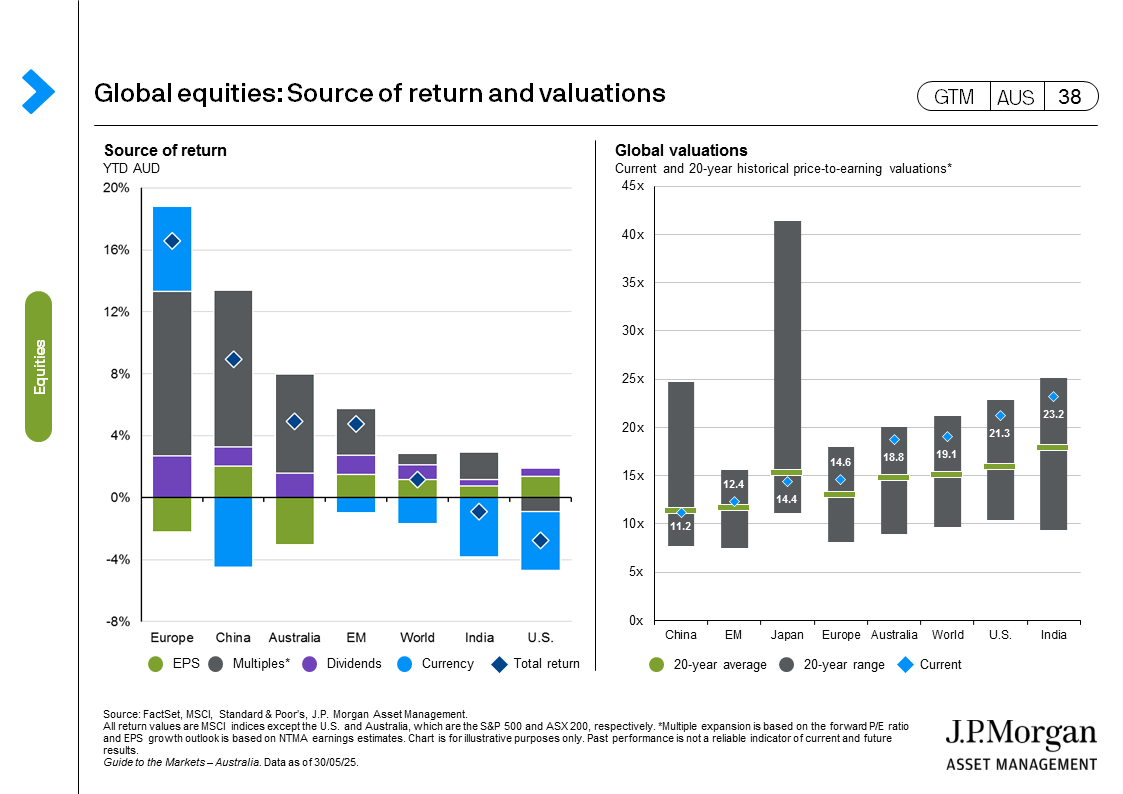

- The MSCI AC World gained 5.7% in May, with most developed markets delivering positive returns in local currency total return terms. Broad-based strong 1Q earnings and optimism around improving trade tension aided markets. U.S. markets logged the strongest returns, followed by European markets and then the Japanese market.

(GTM AUS page 37) - Emerging markets rose 3.2% over the month, with APAC ex-Japan up 4.0% in local currency total return terms, as China rallied on the de-escalation in trade tensions after the Geneva meeting with the U.S. Most other Asian markets were also resilient as trade deal negotiations with the U.S. continues.

- Equity valuations extended in the U.S., with the forward price-to-earnings (P/E) ratio on S&P 500 rising to 21.3x. Valuations on other developed markets also increased, with the ASX 200 at 18.8x, MSCI Europe at 14.6x, and MSCI Japan at 14.4x, which remains below its long-term average.

(GTM AUS page 38)

Fixed income

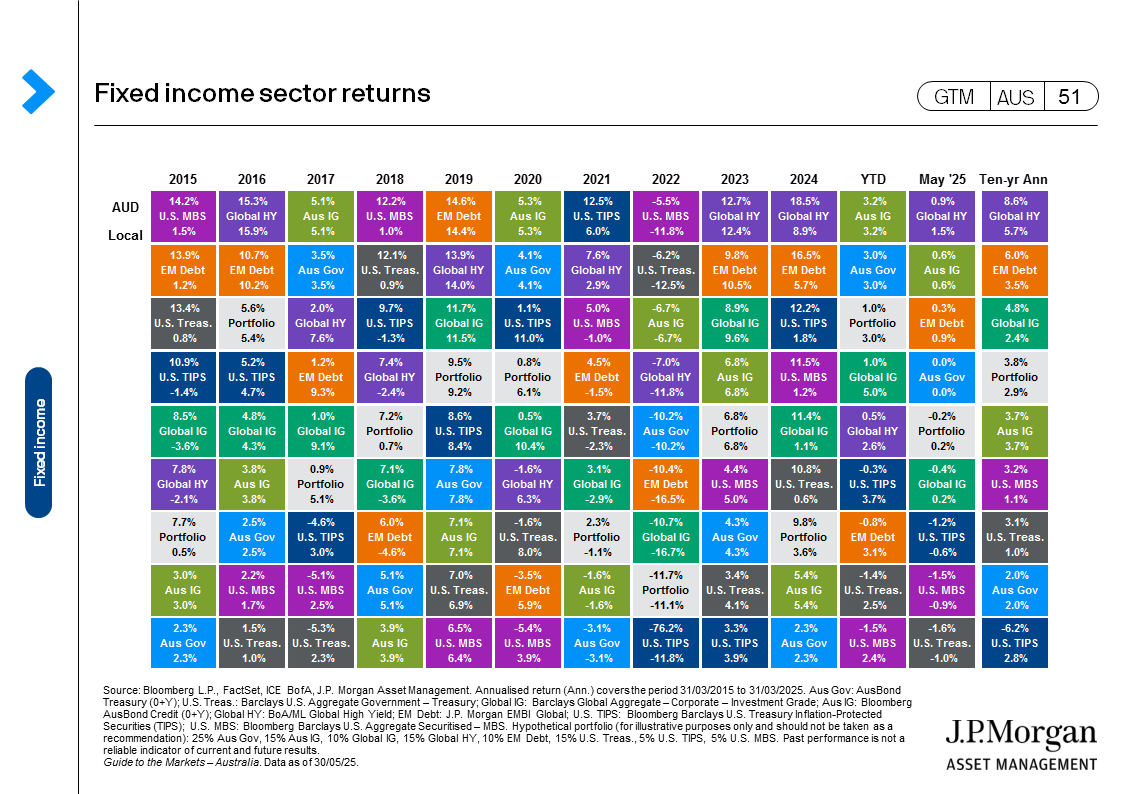

- 10-year yields on Australian government bonds rose 16 bps to 4.27% over the month, though government bond yields in other developed markets increased sharply as well. 10-year yields on U.S. Treasuries were up 24 bps to 4.39%, with 30-year yields testing the 5%-mark, as markets are increasingly concerned over significant fiscal deterioration induced by the reconciliation bill’s tax cuts and extensions, alongside Moody’s rating downgrade.

- Japanese government bond yields also rose over the month, with the 10-year yield at 1.50% and the 30-year yield at a record high of 2.92%, as domestic pressure to ease fiscal policy was met with the BoJ’s purchase tapering and weak auctions. Fiscal pressure also contributed to 30-year yields on UK Gilts and German Bunds reaching decade level highs, on top of the hotter-than-expected inflation print and the Dutch pension reform, respectively.

- Spreads on global high yield bonds narrowed more than on investment grade bonds, returning 1.5% and 0.2% over the month, respectively.

(GTM AUS page 51)

Other assets

- Gold prices edged down 0.7% in May to USD 3,278/oz, while silver and copper prices rose 2.7% and 1.4%, respectively. Crude oil prices fell to USD 62.8/bbl despite the potential OPEC+ production hike.

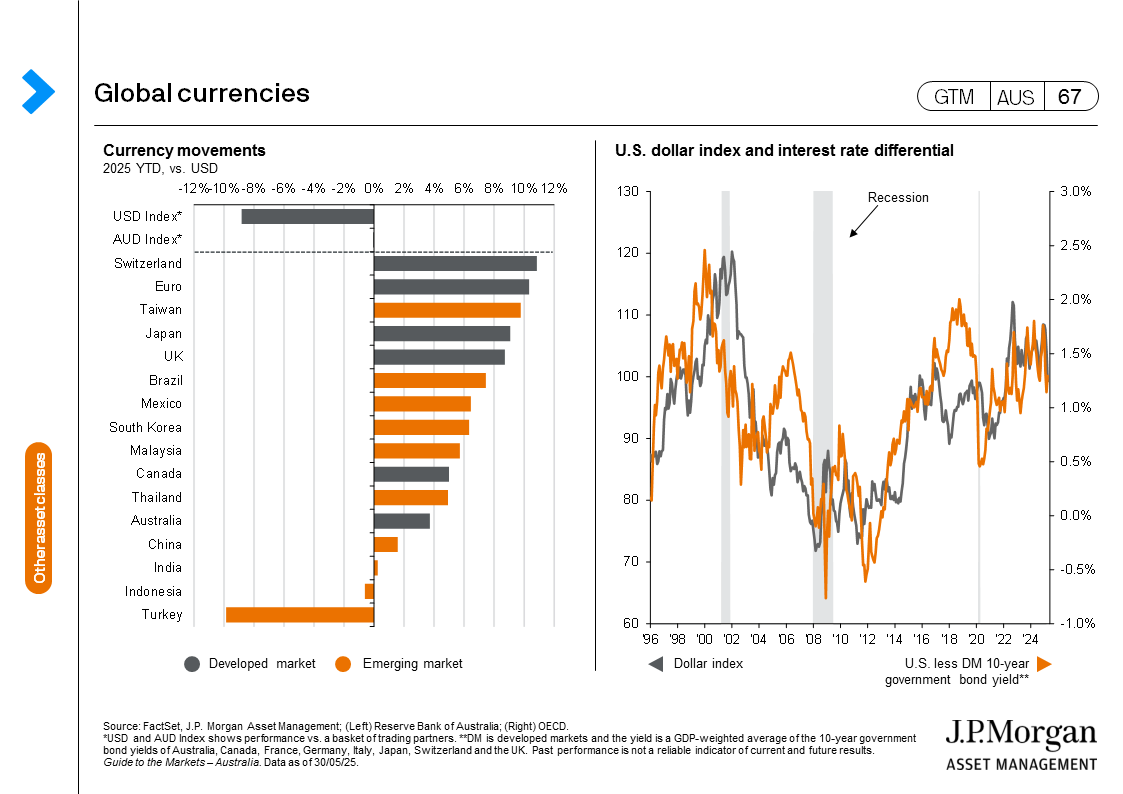

(GTM AUS page 62, 65) - The USD was mostly unchanged over the month, with the DXY index steady at 99.3 by the end of May. While the euro and Japanese yen weakened, most other Asian currencies, such as the Chinese yuan, Australian dollar, Korean won and Taiwanese dollar, had all appreciated against the USD.

(GTM AUS page 67)