A summary of the latest trends in the markets (May 2025)

April was an extremely turbulent month for both global bonds and equities, particularly in the U.S. President Trump’s April 2nd “reciprocal” tariff announcements shocked the world, with tariffs on some partners rising to above 50% along with a 10% universal tariff. However, after the government announced a 90-day pause, markets sharply reversed. However, U.S. equities continued to lag behind ex-U.S. equities, which rose by 4%. Global yields fell 16bps due to rising growth concerns and further central bank cuts in markets like the Eurozone.

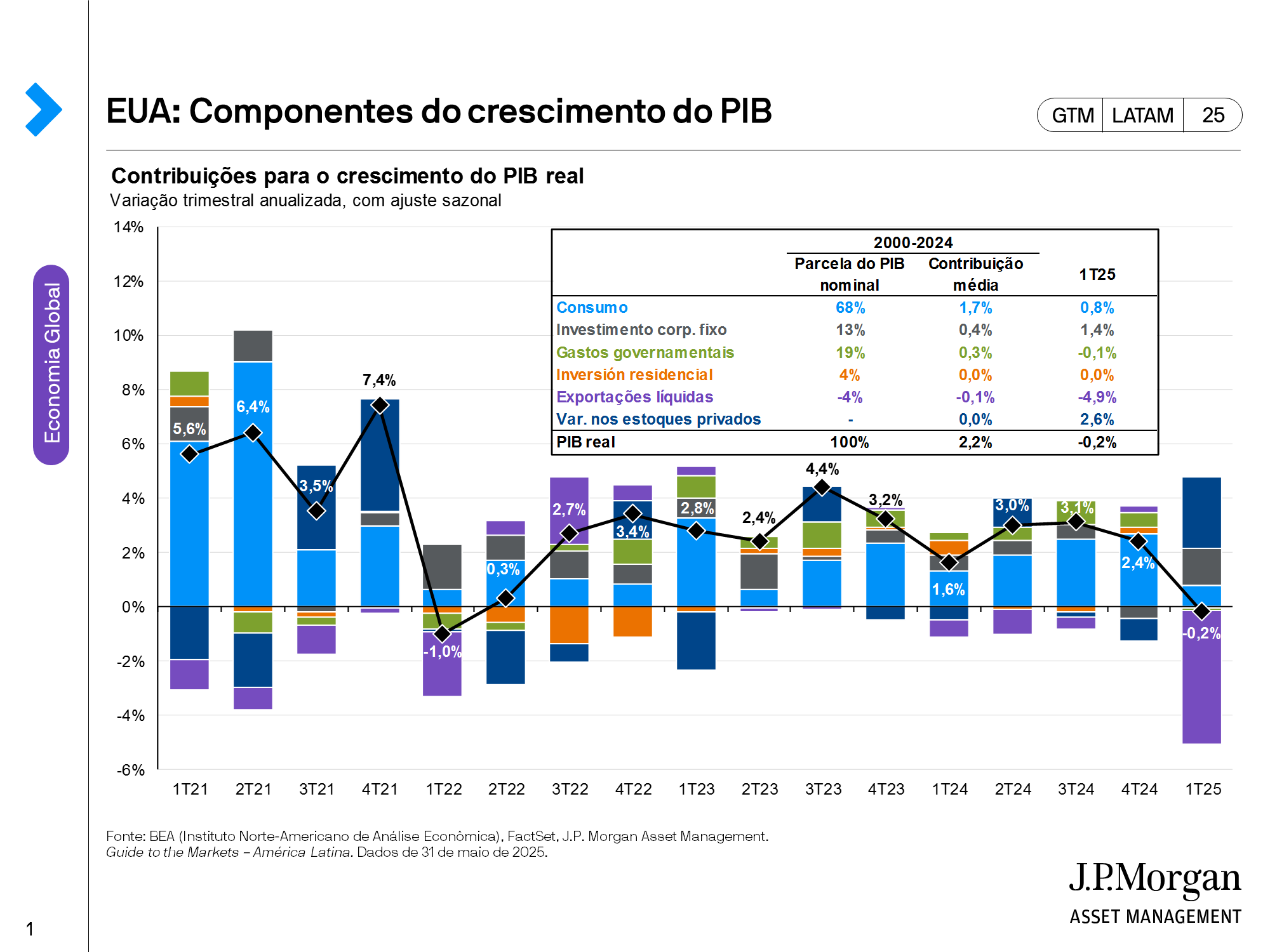

In the U.S., economic indicators are showing early signs of stress. 1Q25 GDP weakened significantly from last quarter (0.3% q/q saar) due to weaker consumption and business investment and a surge in imports. Imports increased due to order frontloading, which could continue, especially for that remain exempt from tariffs for now. Additionally, the U.S. composite PMI was better-than-expected at 51.2, but there was weakness beneath the surface. Domestic orders picked up likely due to buyers trying to find domestic alternatives, but new export orders, or orders from abroad, dropped 3.9pts to 47.2. Lastly, March’s headline CPI was 2.4% y/y (-0.1% m/m), marking the first m/m drop since May 2020. While a decrease in inflation is welcome, it may also indicate weakening consumer demand, as more sensitive sectors, such as airline tickets, are experiencing more pronounced declines.

The International Monetary Fund (IMF) published its revised 2025 growth forecasts, which were notably weaker than its last revision in October 2024. Unsurprisingly, the U.S. experienced one of the most significant growth downgrades since last October, from 2.7% to 1.8% in 2025. There were also large downward revisions for countries dependent on U.S. exports, such as Mexico (1.4% to -0.3%), South Korea (2.0% to 1.0%), Vietnam (6.1% to 5.2%), and Canada (2.0% to 1.4%). While domestic factors contributed to the downgrades as well, trade tensions and policy uncertainty were key considerations.

Volatility dominated markets throughout April. President Trump announced unexpectedly large tariffs on most of the U.S.'s trading partners, with some facing tariffs above 50%, depending on the size of the trade deficit, alongside 10% universal tariff. This announcement came just days after he had described that the tariffs would be "lenient," leading to further market shock. In response to the ensuing market turmoil and political pressure, Trump announced a 90-day pause on the tariffs. He also exempted products containing semiconductors, such as smartphones, due to the heavy reliance on imports from countries like China.

The trade war with China escalated significantly, with the U.S. imposing a 145% tariff on most Chinese imports, prompting China to retaliate with similar measures. The on-again, off-again tariffs sparked extreme market volatility. Following the announcements, U.S. equities plummeted by a staggering 12% over four trading days, with most other markets also experiencing declines. However, after the 90-day pause was announced on April 9th, markets rebounded sharply, with the S&P 500 increasing by 10% in a single trading day, marking the best day for U.S. equities since October 2008, while the tech-heavy Nasdaq had its best day since January 2001.

The Treasury market was not exempt from the volatility either. The U.S. 10-year Treasury yield touched a low of 3.87% on April 4th and shot up to 4.50% in a few days, a near 60bps swing in a very short window. Potential factors behind this move include concerns about waning foreign demand of U.S. Treasuries, general economic uncertainty, and the basis trade unwinding. However, the basis trade—where traders short Treasury futures and go long on cash bonds—was likely not the source, but rather an exacerbating factor. Also, it will be important to monitor is Treasury selling by trade partners rises as a potential retaliation tactic.

In April, the U.S. dollar also faced significant headwinds. The White House made several remarks aimed at pressuring the Fed to lower interest rates and even discussed potentially terminating Chair Powell’s term early. While the president does not have the full power to do this, these comments raised concerns about Fed independence. As a result, the U.S. dollar plunged and is down 8% year-to-date. So far this year, the dollar has depreciated 10% against the Euro and 7% vs. GBP. Emerging market currencies, such as the Brazilian real and Mexican peso, have also strengthened significantly. Given the dollar’s 15+ year run-up, it may have farther to fall if policy uncertainty remains at such elevated levels.

So, what’s the investing playbook amid the trade turmoil? Investors can bolster portfolios with global core bonds, which have historically helped during growth shocks and are already up 5% YTD. Liquid alternatives can also help investors diversify quickly. Within equity portfolios, investors should consider increasing exposure to high quality, fairly valued companies with a focus on markets like Japan and Europe. Companies with high valuations, like the Mag 7, have been leading the downturn, and analysts are expected to continue revising 2025 earnings estimates downward, reflecting greater macro uncertainty. Also, active management can separate the winners from the losers: companies that are domestically oriented, services-oriented and have higher pricing power are likely to fare better. However, significant portfolio adjustments are likely note necessarily for most investors. Adhering to an investment plan, including regular rebalancing and goal-based adjustments, remains the most effective long-term strategy.

For important information, please refer to the homepage.

This content is intended for qualified investors and is part of the educational material available for download through this page. We recommend reading the document for complete access to the information and its respective disclaimers.